Step 2. Lender Choice & Pre-Approval in The Buying Process

The choice has been made; you’re buying a home! Congrats! Now, comes the “fun part”. Starting the home buying process continues with one of the more confusing parts of process for new buyers: lender choice & pre-approval. It is a standard in the real estate process for buyers to have a pre-qualification letter from a certified lender before any offer is taken seriously, so attaining this documentation is a must for a quick process. This approval process will include the vetting of sensitive information such as W2s, employment verification and bank accounts. Working with a trusted lender can make this process more streamlined and stress-free. Here are some tips for choosing the best lender for every situation and attaining a pre-approval letter.

The choice has been made; you’re buying a home! Congrats! Now, comes the “fun part”. Starting the home buying process continues with one of the more confusing parts of process for new buyers: lender choice & pre-approval. It is a standard in the real estate process for buyers to have a pre-qualification letter from a certified lender before any offer is taken seriously, so attaining this documentation is a must for a quick process. This approval process will include the vetting of sensitive information such as W2s, employment verification and bank accounts. Working with a trusted lender can make this process more streamlined and stress-free. Here are some tips for choosing the best lender for every situation and attaining a pre-approval letter.

The Formula for Success

The best formula for success includes three steps in the process:

Trust + Service + Loan Estimate = Best Loan Choice

Trust

Lenders and loan officers will be working side by side with the buyer throughout the entire home buying process and will be handling sensitive personal information about your family and financial wealth. No one wants to give this information to someone they do not completely trust. A good adage to choosing the best lender is to find someone with the heart of a teacher; someone that will work to ensure best program is available to the buyer and answer all questions. This lender should be someone that cares about your financial situation and works to be a cheerleader throughout the entire process. Find a lender that cares about buyer success and can answer the following questions accurately and with ease:

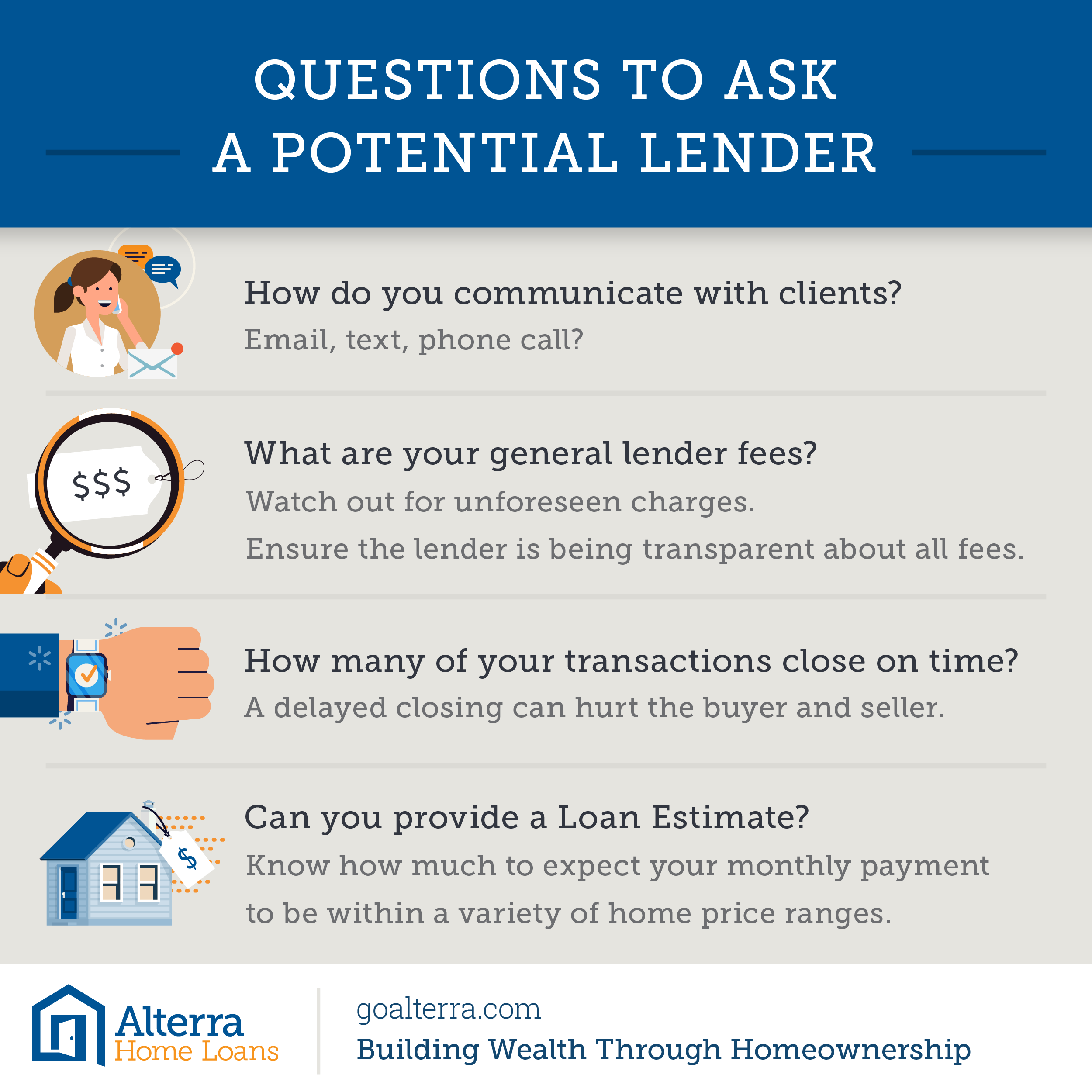

-How will the lender communicate with you? Ideally the response will include 2-3 forms of communication: email, portals and phone communication.

-What are the general lender fees? Some lenders will tact unforeseen charges onto the loan. Be vigilant and ensure that the lender is being transparent about all fees.

-How many of the lender’s transactions close on time? A delayed closing can hurt the buyer and seller.

-Are loan officers paid by salary or commission? Often, commission-based lenders will often provide better service because their income depends on receiving a quick and accurate closing. Your successful closing is their successful closing.

-Can they provide a Loan Estimate? This is an important question in the process and will be discussed more at the end of this commentary.

Service

Customer service should be the highest priority to any lender before their bottom line. Choose a lender that is accessible and available for you needs. A lender should be able to meet with the you within 48-72 hours of a requested meeting as well as available via phone, text and even after hours. The lender should be straightforward with the buyer throughout the process, even when the information is something the buyer does not want to hear. The lender should be able to articulate the entire buying process with ease to the buyer and work with the buyer to choose the best loan options in addition to pre-approval assistance.

Loan Estimate

Coming full circle to trust factor above, receiving an accurate and competitive loan estimate is a must from lenders. A loan estimate helps you know exactly how much your monthly payment is estimated to be within a variety of home price ranges. This is critical to a successful home search. An inaccurate loan estimate can have buyers searching for homes that are unattainable, leading to heartbreak or stretching families financially.

At the end of the day, the lender any buyer deserves is one that is upfront, efficient and interested in a successful, on-time closing, not the rate of the loan. The lowest rate is not always the best loan option, so a trusted lender can assist buyers in weeding through the process of determining the best loan. Exceptional service from lenders can make the entire process a simple one for buyers.

Still on the Fence About Buying?

“Even if you’re on the fence about if homeownership is right for you, you should meet with a loan officer and discuss options. Often, the issue is that people are not sure about their credit. But generally, if you’ve been working for the last two years and have decent credit, you can get into a home.” Jaime Tapia, Area Manager, Alterra Home Loans (Los Angeles)

Now that a pre-approval letter and the best loan options have be attained, it is time to pick the next partner in the home buying journey: the real estate agent.

By: https://www.bhgre.com/bhgrelife/step-2-lender-choice-pre-approval-in-the-buying-process |The BHGRE Life Blog